.png)

Overview

This professional strategy is designed for H1 (1-hour) timeframes, combining trend identification, volatility measurement, and volume confirmation without relying on conventional oscillators such as RSI, MACD, or Stochastic. It provides a structured approach suitable for both manual discretionary traders and algorithmic EA developers, aiming for consistent risk-adjusted returns under varying market conditions.

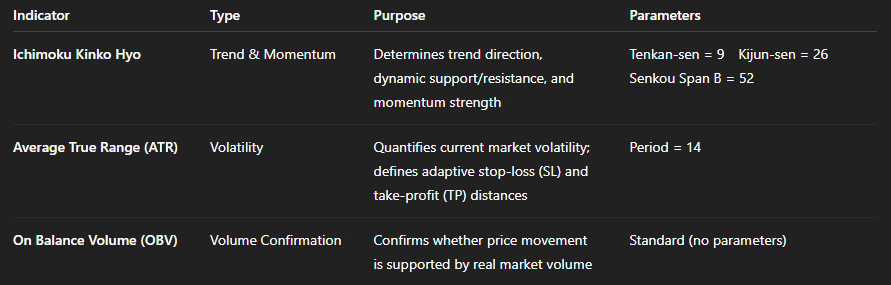

Used indicators and parameters:

Trend Identification – Ichimoku Cloud (Kumo)

Before entering any trade, define the overall trend using the Kumo Cloud:

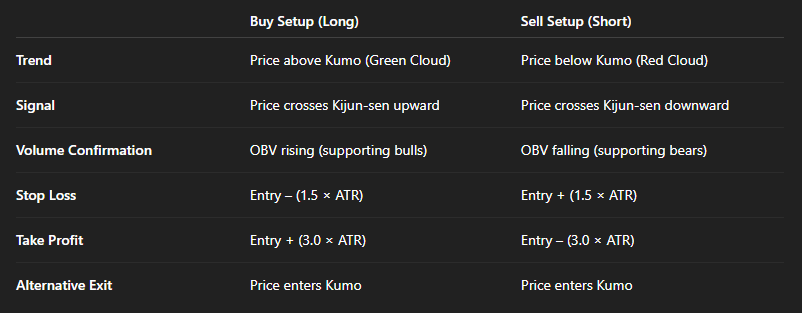

- Bullish Trend (Long Bias): Price candles are above the Kumo and the cloud is green (Senkou Span A > Senkou Span B).

- Bearish Trend (Short Bias): Price candles are below the Kumo and the cloud is red (Senkou Span A < Senkou Span B).

- Neutral / Ranging Market: Price is inside the Kumo — avoid trading until a clear break occurs with momentum confirmation.

Entry Conditions

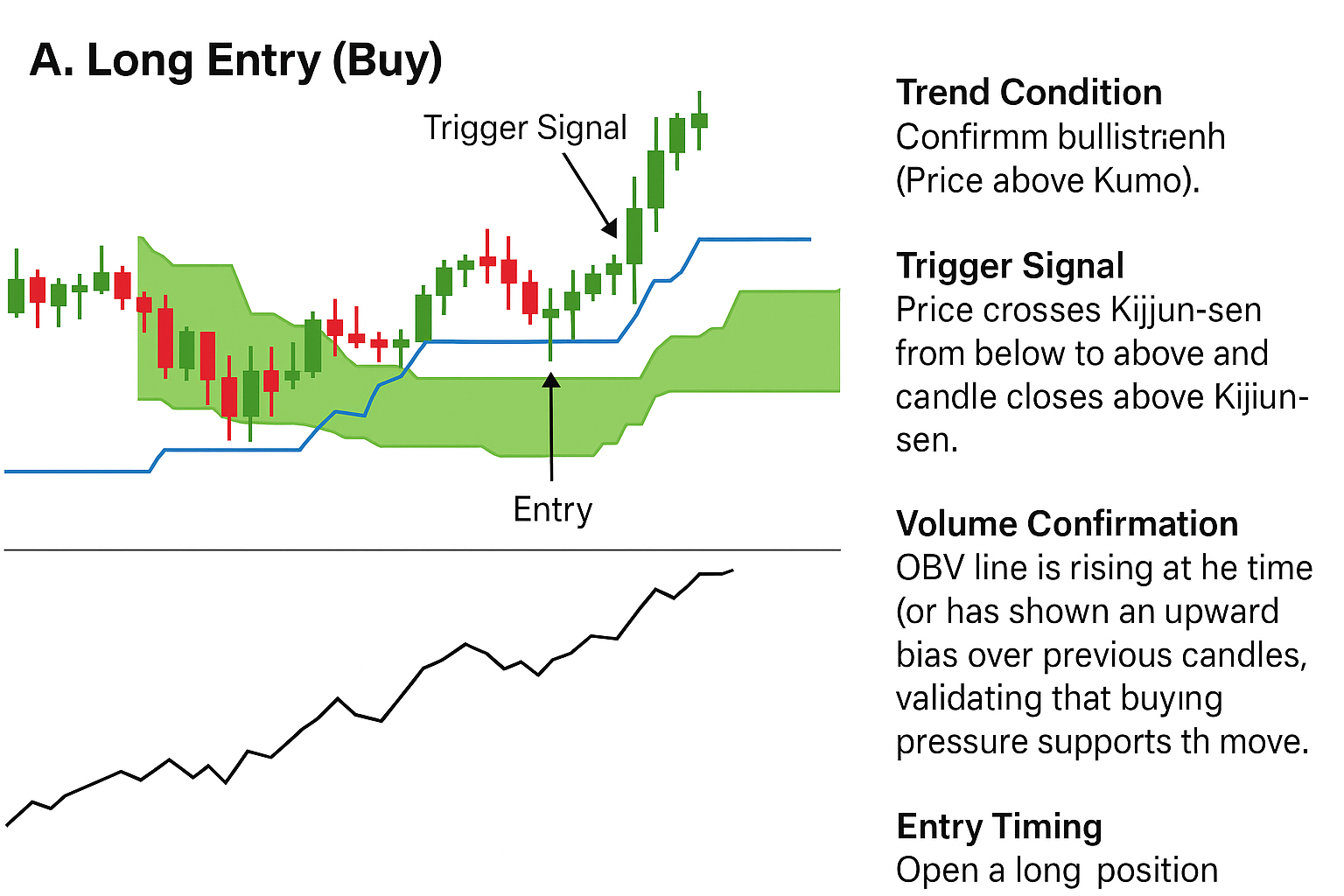

Long Entry (Buy)

- Trend Condition: Confirm bullish trend (Price above Kumo).

- Trigger Signal: Price crosses Kijun-sen from below to above and the candle closes above the Kijun-sen.

- Volume Confirmation: OBV line is rising at the same time (or has shown an upward bias over previous candles), validating that buying pressure supports the move.

- Entry Timing: Open a long position at the opening price of the next candle after the signal.

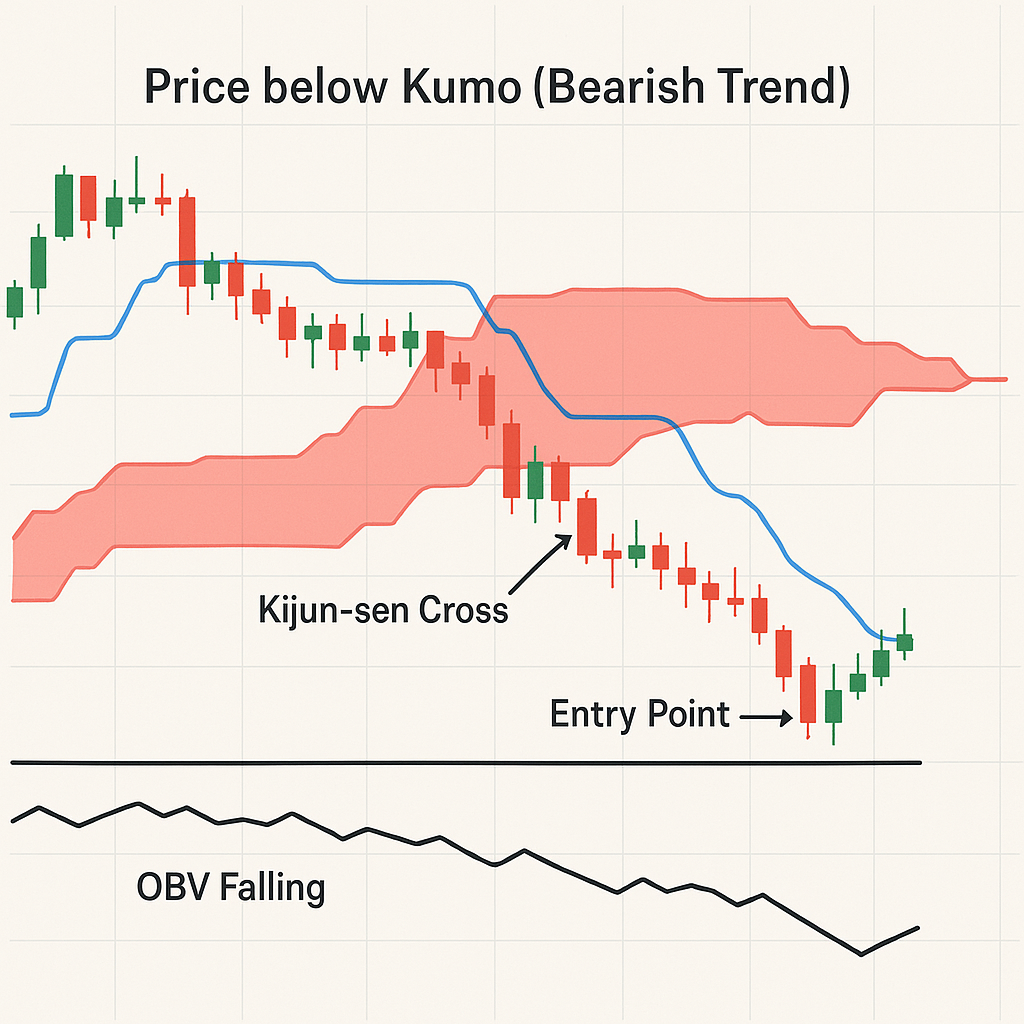

Short Entry (Sell)

- Trend Condition: Confirm bearish trend (Price below Kumo).

- Trigger Signal: Price crosses Kijun-sen from above to below and the candle closes below the Kijun-sen.

- Volume Confirmation: OBV line is declining (or has been trending downward), validating that selling pressure supports the move.

- Entry Timing: Enter short on the next candle’s open after the signal.

Risk Management via ATR

ATR dynamically adjusts stop-loss and take-profit distances based on current volatility, maintaining consistent risk/reward across various market conditions.

Calculation Rules

- Measure ATR Value: At the moment the entry signal is confirmed, record the current ATR (14) value.

- Stop Loss (SL):

- Distance: 1.5 × ATR

- For Long Trades: SL = Entry Price – (1.5 × ATR)

- For Short Trades: SL = Entry Price + (1.5 × ATR)

- Take Profit (TP):

- Distance: 3.0 × ATR

- For Long Trades: TP = Entry Price + (3.0 × ATR)

- For Short Trades: TP = Entry Price – (3.0 × ATR)

This provides a 1 : 2 risk-to-reward ratio, ensuring a mathematically favorable expectancy even with a win rate below 50%.

Exit Rules

Trades close under one of the following scenarios:

- TP or SL Hit: Position closes automatically upon reaching the predetermined levels.

- Trend Reversal: Price moves into the Kumo cloud or closes on the opposite side of the cloud, indicating a loss of momentum or trend change.

- Opposite Signal: An inverse Ichimoku Kijun-sen cross forms (e.g., a sell signal during an existing buy trade).

Example scenarios:

Additional Optimization & Tips

- Time Filters: Avoid low-liquidity periods (e.g., Asian session for XAUUSD pairs).

- Pair Selection: Best results with major pairs and gold (XAUUSD), where OBV volume correlates well with price momentum.

- ATR Adaptation: Re-optimize ATR period (10 – 20) to match volatility of different assets.

- Partial Take Profit: Secure ½ position at 1.5×ATR and trail the remainder with a Kijun-sen or custom ATR trailing stop.

- Backtesting: Recommended minimum 100 trades for statistical reliability and forward testing under live market conditions.

Advantages

- Pure price + volume + volatility logic (no lagging oscillators)

- Dynamic risk control adapting to market conditions

- Suitable for both trend-following and swing approaches

- Clear entry/exit mechanics for automation (EA development)

This strategy integrates Ichimoku’s multi-dimensional trend framework, ATR’s volatility filter, and OBV’s volume confirmation into a coherent trading model for the H1 timeframe. When implemented with disciplined risk management and psychological control, it can serve as a robust foundation for consistent profitability and further AI-assisted optimization.