.png)

Understanding futures markets can be challenging, especially when one encounters terms like Backwardation. In this article we’ll dive deep into what backwardation is, why it matters, its causes, how it differs from its opposite (contango), and what implications it has for traders, hedgers and investors. By the end, you’ll have a clear picture of this sometimes-puzzling market structure.

What is Backwardation?

At its core, backwardation describes a futures market structure in which the current or near-term spot price of an asset (or commodity) is higher than the price of futures contracts set for delivery at a later date. In simpler terms: you pay more now than you will for later delivery.

From several sources:

- According to Investopedia: “Backwardation occurs when the current price, or spot price, of a commodity is higher than the prices in the futures market.”

- From CME Group: “When a market is in backwardation, the forward price of the futures contract is lower than the spot price.”

- From IG UK glossary: “Backwardation is the market condition in which the price of a futures contract is currently trading lower than the spot price of the underlying.”

Visually you can imagine a futures curve (price vs maturity) that slopes downward: near‐term contracts are higher than later ones.

Because this is less typical than the upward slope (contango) in many markets, backwardation stands out and signals particular market dynamics.

Why Does Backwardation Occur?

Several underlying forces might push a market into backwardation. Here are the most prominent:

1. Supply shortages / strong immediate demand. When the spot market is tight (e.g., commodity supply is constrained, inventories are low, demand is high right now), buyers are willing to pay a premium for immediate delivery rather than wait for a future contract. This raises the spot (or near term) price relative to later-dated contracts.

2. Convenience yield. In commodity markets (especially physical ones), holding the physical asset can provide benefits — called the “convenience yield” (for example, ensuring production continues, avoiding disruption, guaranteeing supply). When inventory is low, convenience yield is high, which may push spot price above the futures price.

3. Expectations of falling future prices. If the market expects future prices to decline (due perhaps to increased supply, weaker demand, or other factors), futures contracts may price in that expectation — making the later delivery price lower relative to today.

4. Carrying costs and storage. In the normal case, futures prices are higher than spot to reflect cost of carry (storage, insurance, financing) – this leads to contango. But when carrying the asset yields less benefit (or storing is difficult/expensive) and convenience yield is high, the futures price may drop below spot, which helps explain backwardation.

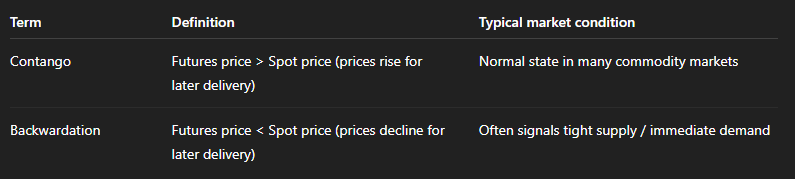

Backwardation vs Contango – The Contrast

Understanding backwardation is easier when contrasted with its counterpart: Contango.

How Does Backwardation Work in Practice?

Let’s walk through a simplified example to illustrate backwardation:

- Suppose a commodity’s spot price today is $100.

- A futures contract for delivery in three months is trading at $90.

- That means the market is in backwardation — because you could theoretically buy the futures contract for $90 and, if you’re able to get delivery, you have a contract cheaper than what you would pay if you bought the commodity today.

From this situation, one might expect:

- Some participants might sell the physical commodity at the current higher price ($100), and buy the futures contract at $90 (if delivery is possible) to lock in the future delivery cheaper.

- Over time as the contract approaches maturity, the futures price and spot price will converge (as arbitrage opportunities vanish) — standard futures theory.

- The downward relation between spot and futures reflects that current demand is strong relative to future expected demand or supply.

Another practical especially in commodities: if supply is constrained now (e.g., weather event affecting crops, or physical shipment delays) the spot price may spike. Participants who need immediate delivery pay a premium. The future months may be priced lower because supply is expected to normalise later.

Implications for Traders, Hedgers and Investors

Understanding the backwardation structure helps market participants in several ways:

For Hedgers

- Producers who need to hedge may prefer futures contracts. In backwardation, futures prices are lower than spot now, so hedging may look less attractive if the spot premium is high.

- Users needing the commodity (consumers) may prefer securing physical supply now rather than relying purely on futures.

For Speculators

- Backwardation can create opportunities for profit (roll yields) in commodities ETFs/futures rolling: buying a contract at $90 and delivering at $100 (or the spot ends up higher) can be profitable if managed properly.

- But risks remain: expectation of price drop or supply restoration may mean futures fall further.

For Inventory/Storage Decisions

- When the market is in backwardation, it reduces the incentive to hold inventories for later because near-term price is high relative to futures – it may be better to sell now than store.

- Conversely, in contango one might store for future delivery. This dynamic is key in physical commodity markets.

Market Sentiment Indicator

- Backwardation often signals that the market expects lower supply or higher demand in the short term (thus near term premium).

- It can also indicate the market expects future supply to improve (thus lower future price) or demand to weaken.

- Therefore, the shape of the futures curve (backwardation vs contango) provides insight into market expectations.

Examples and Real-World Context

Here are some contexts where backwardation has appeared:

- Commodity markets (oil, natural gas, agricultural products) see backwardation when there’s a physical shortage or surge in demand. For example, IG UK notes: “The natural gas futures market is often in backwardation as it sees increasing demand in the winter months and shortages in supply.”

- The Wikipedia page on “Normal backwardation” explains that historically multiple commodities have exhibited backwardation due to seasonal issues, inventory constraints, etc.

- The notion of “inverted market” (which overlaps conceptually with backwardation) often arises when spot price and near-maturity contracts exceed farther‐term ones due to immediate supply constraints.

Why Backwardation Matters for You (Especially if you’re involved in Markets)

Since you’re interested in trading, education and signals (particularly in Forex and commodities), backwardation is a concept worth mastering. Here’s why:

- If you trade commodity futures or ETFs that track them, the shape of the curve (backwardation vs contango) influences returns, especially when rolling contracts.

- In Forex and cross-asset contexts, the same logic of “future price relative to spot” influences pricing, though less visibly than in physical commodities.

- Understanding backwardation helps you interpret market signals: if a commodity you follow moves into backwardation, it may signal tight near-term supply or elevated demand — potential trade setups.

- From a risk perspective: knowing that a market in backwardation may reflect short-term supply stress means you’re alert to the possibility of sudden reversals if supply/demand assumptions change.

Limitations and Things to Watch

While backwardation is a powerful concept, here are some caveats and important considerations:

- Not always profitable: Just because a market is in backwardation doesn’t guarantee profits for every participant. Speculators still have to manage risk, timing, and roll costs.

- Expectations can change: If the market’s expectation of future supply/demand shifts, the curve might flip into contango. Your positions must adapt.

- Storage, delivery and physical constraints matter: The concept is more salient in real commodities with physical delivery/storage issues. In purely financial futures the intuition may weaken.

- Data access: To assess backwardation you need reliable futures curve data across maturities — not always trivial for certain assets or regions.

- Not all downward slopes mean the same thing: Sometimes a downward slope arises from anticipated weakening demand rather than supply scarcity — the trade logic differs. For instance, backwardation might reflect expectation of falling future price rather than current scarcity.

Summary & Key Takeaways

To wrap up:

- Backwardation occurs when the spot price (or near-term contract) is higher than the futures price for later delivery.

- It often signals strong immediate demand or supply constraint (or expectation of weaker future demand or stronger future supply).

- It opposes contango, which is where futures are priced higher than spot because carrying costs and positive carry dominate.

- For traders, hedgers and investors the futures‐curve shape (backwardation vs contango) carries actionable information about market structure and expectations.

- While insightful, it is not a guarantee of profit — change your assumptions, and the structure may flip.

- As someone involved in trading education, explaining backwardation adds sophistication and helps your audience understand deeper market dynamics beyond just “price up/down”.