.png)

In the modern financial landscape, market movements are no longer solely dictated by economic fundamentals or technical analysis. A new, powerful force has emerged from the complex world of derivatives: the Gamma Squeeze. This phenomenon, which gained mainstream notoriety during the retail trading frenzy of 2021, represents an explosive feedback loop between options trading and the underlying asset's price, leading to rapid, dramatic shifts in valuation. While the Gamma Squeeze is most commonly discussed in the context of the stock market, its underlying mechanics—driven by the hedging activities of market makers—are equally relevant to the foreign exchange (Forex) market, particularly in the realm of currency options and their impact on currency pairs like EUR/USD or USD/JPY.

This comprehensive guide will demystify the Gamma Squeeze, explain the crucial role of the Options Greeks, detail the step-by-step mechanics of the squeeze, and analyze its implications for Forex traders navigating periods of extreme market volatility.

The Foundation: Options, Market Makers, and Hedging

To understand the Gamma Squeeze, one must first grasp the roles of options and the entities that facilitate their trading.

1. The Role of Options

An option is a derivative contract that gives the holder the right, but not the obligation, to buy (a call option) or sell (a put option) an underlying asset at a specified price (strike price) on or before a certain date (expiration date).

2. The Market Maker's Dilemma

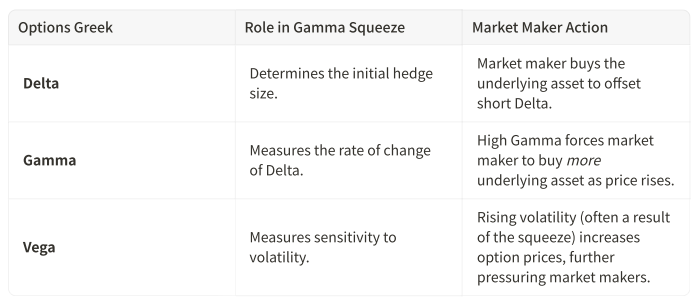

Market makers are financial institutions that provide liquidity by simultaneously quoting both a buy and a sell price for an option. When a market maker sells a call option to a trader, they take on a short position in the option. This exposes them to risk: if the underlying asset's price rises sharply, the call option they sold will become valuable, leading to a loss. To maintain a delta-neutral position—meaning their portfolio's value is insulated from small movements in the underlying asset's price—market makers must hedge their risk. When they sell a call option, they must buy a corresponding amount of the underlying asset (e.g., shares of a stock or a specific amount of a currency pair) to offset the risk. This hedging activity is the engine that drives the Gamma Squeeze.

The Options Greeks: Delta and Gamma

The mechanics of the squeeze are governed by two of the Options Greeks, which are measures of an option's sensitivity to various factors.

Delta ($\Delta$)

Delta measures the sensitivity of an option's price to a $1 change in the price of the underlying asset.

- A call option with a Delta of 0.50 means the option's price will increase by $0.50 for every $1 increase in the underlying asset's price.

- More importantly for hedging, Delta also represents the theoretical amount of the underlying asset a market maker must hold to remain delta-neutral. If a market maker sells 100 call options with a Delta of 0.50, they must buy 50 units of the underlying asset to hedge.

Gamma ($\Gamma$)

Gamma is the key to the squeeze. It measures the rate of change of an option's Delta relative to a $1 change in the underlying asset's price. In simpler terms, Gamma tells the market maker how much their hedge needs to change as the price moves.

- Gamma is highest when an option is At-The-Money (ATM) and decreases as the option moves In-The-Money (ITM) or Out-of-The-Money (OTM).

- A high Gamma means that a small movement in the underlying price causes a large change in Delta, forcing the market maker to adjust their hedge aggressively.

The Mechanics of the Gamma Squeeze

A Gamma Squeeze is a self-reinforcing cycle of buying pressure that occurs when a large volume of traders buy call options, forcing market makers to buy the underlying asset to hedge, which in turn pushes the price up, forcing them to buy even more. The process unfolds in four critical steps:

- Step 1: The Initial Spark (Call Buying)

The squeeze begins with a significant, concentrated buying of call options, often by retail traders or large institutions, typically targeting options that are Out-of-The-Money (OTM) but close to the current price. This buying pressure is often speculative, betting on a rapid price increase.

- Step 2: Market Maker Hedging (Delta-Hedging)

When market makers sell these call options, they are now "short Gamma" and "short Delta." To become delta-neutral, they must buy the underlying asset. This initial buying pressure pushes the price of the underlying asset slightly higher.

- Step 3: The Gamma Feedback Loop

As the price of the underlying asset rises, the OTM call options move closer to the strike price and become At-The-Money (ATM). This is where Gamma is highest.

- Because of the high Gamma, the Delta of the options increases rapidly.

- The market maker's required hedge (the amount of the underlying asset they need to hold) increases dramatically.

- To maintain their delta-neutral position, the market maker is forced to buy more of the underlying asset.

- Step 4: The Squeeze and Exponential Price Rise

This forced buying by market makers creates a massive, non-fundamental demand for the underlying asset. This demand pushes the price even higher, which further increases the options' Delta and Gamma, forcing the market makers to buy even more. This positive feedback loop is the Gamma Squeeze, resulting in an exponential, parabolic price move and extreme market volatility.

Gamma Squeeze in the Forex Market

While the Gamma Squeeze is primarily associated with equity markets, the same principles apply to the foreign exchange market through currency options. Major currency pairs like EUR/USD, USD/JPY, and GBP/USD all have active options markets, and the hedging activities of large banks and institutions can create similar, albeit often less dramatic, squeeze events.

The Mechanism in Currency Pairs

- Options Open Interest: Large concentrations of open interest in call or put options for a specific currency pair (e.g., call options on EUR/USD at a specific strike price) create a "Gamma Wall" or "Gamma Barrier."

- Hedging Flows: If the spot price of the currency pair approaches this strike price, the market makers who sold those options must hedge their exposure by buying or selling the underlying currency pair in the spot Forex market.

- The Squeeze: If the price breaks through the Gamma Wall, the forced hedging flows (buying the currency pair to hedge short calls, or selling to hedge short puts) can accelerate the move, causing a sharp spike in the exchange rate.

Relevance for Forex Traders

For the typical Forex trader who deals only in the spot market, the Gamma Squeeze is not a direct trading strategy but a critical factor in understanding unexpected market volatility.

- Expiration Dates: Large options positions often expire on specific dates (e.g., monthly or quarterly), and hedging activity tends to peak in the days leading up to these expirations. Traders should monitor the options expiration calendar for major currency pairs to anticipate potential spikes in volatility.

- Technical Levels: Options strike prices often cluster around significant psychological or technical analysis levels (e.g., 1.1000 for EUR/USD). A break of these levels can trigger a Gamma Squeeze, turning a minor breakout into a parabolic move.

- Risk Management: The squeeze can cause rapid price dislocation, leading to wider spreads and increased slippage. Risk management becomes paramount, requiring tighter stop-loss orders or a temporary reduction in leverage during high-risk periods.

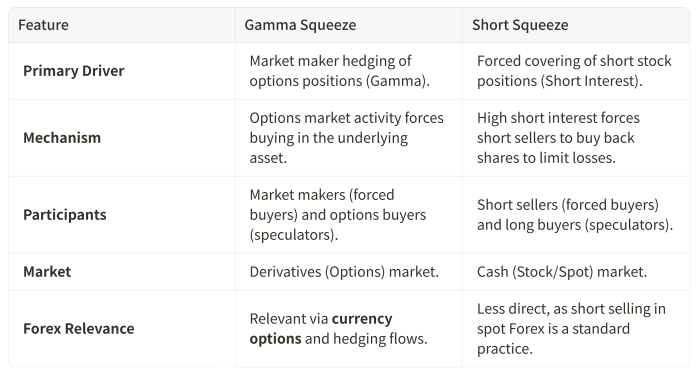

Distinguishing Gamma Squeeze from Short Squeeze

It is crucial to differentiate the Gamma Squeeze from the more widely known Short Squeeze, although they often occur simultaneously and reinforce each other.

In the famous GameStop event, the initial surge was a Short Squeeze (short sellers covering), which then triggered a massive Gamma Squeeze (market makers hedging the influx of call options), creating a powerful, combined effect.

The Future of Gamma: Dealer Positioning and Market Stability

The concept of Gamma is now a core component of advanced quantitative analysis. Traders and analysts monitor "Dealer Gamma Positioning" to gauge the overall stability of the market.

- Positive Gamma: When market makers hold a net long Gamma position, they are generally net sellers into rallies and net buyers into dips. This acts as a stabilizing force, dampening market volatility and keeping prices range-bound.

- Negative Gamma: When market makers hold a net short Gamma position (often due to heavy call buying), they must buy into rallies and sell into dips. This creates a destabilizing, self-reinforcing feedback loop, making the market highly susceptible to a Gamma Squeeze.

Understanding this positioning allows traders to anticipate whether the market is likely to be choppy and range-bound (positive Gamma) or prone to sharp, directional moves (negative Gamma).

Conclusion: A New Dimension of Market Analysis

The Gamma Squeeze is a powerful testament to the interconnectedness of the financial markets. It demonstrates how activity in the derivatives market can create massive, non-fundamental price movements in the underlying asset, including major currency pairs. For the modern Forex trader, a comprehensive trading strategy must extend beyond traditional technical analysis and fundamental analysis to include an awareness of options-driven hedging flows. While the mechanics are complex, the takeaway is simple: large concentrations of options open interest at specific strike prices create potential inflection points—Gamma Walls—that, if breached, can unleash a torrent of forced buying or selling, leading to explosive market volatility. By monitoring options expiration dates, identifying key strike price clusters, and understanding the principles of Delta and Gamma, traders can better anticipate these non-fundamental price dislocations, allowing for superior risk management and the potential to capitalize on some of the most dramatic moves the market has to offer.