.png)

In the global financial system, banks often operate across borders, dealing with multiple currencies and clients from different jurisdictions. To manage these transactions efficiently, banks maintain specific types of accounts with one another — known as Nostro, Vostro, and Loro accounts. Understanding these concepts is crucial for professionals in international finance, treasury operations, and foreign exchange trading, as they form the backbone of global banking communication and settlements.

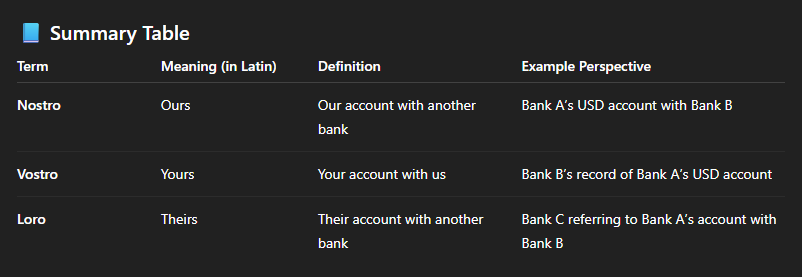

What Is a Nostro Account?

“Nostro” is a Latin term meaning “ours”. A Nostro account refers to “our account with another bank in a foreign country.” In simple terms, it’s an account that a domestic bank holds with a foreign bank, denominated in the foreign currency of that country. This account allows the domestic bank to facilitate international payments, currency conversions, and settlements without relying on intermediaries.

Example: If Bank A (Azerbaijan) holds an account in USD with Bank B (USA), then for Bank A, it’s a Nostro account (our account with you).

Purpose:

- Settling foreign trade transactions

- Facilitating international wire transfers (SWIFT)

- Managing foreign currency liquidity

- Reducing exchange conversion costs

What Is a Vostro Account?

“Vostro” is derived from the Latin word “yours.” A Vostro account means “your account with us.” From the perspective of the foreign bank, the same account that is a Nostro account for Bank A becomes a Vostro account for Bank B.

Example: In the above scenario, Bank B (USA) will record Bank A’s USD account as a Vostro account (your account with us).

Purpose:

- Helps the foreign bank manage funds deposited by overseas banks

- Enables efficient cross-border fund movements

- Supports trade settlement between domestic and foreign entities

Key point: Nostro and Vostro accounts are essentially mirror images of the same account, viewed from opposite perspectives.

What Is a Loro Account?

“Loro” means “theirs” in Latin. A Loro account refers to “their account with you” or “their account with another bank.” It is used when a third bank refers to an account maintained by one bank with another. Loro accounts come into play in multi-bank correspondent relationships, where communication about foreign accounts involves third-party references.

Example: If Bank C (UK) refers to the account that Bank A (Azerbaijan) holds with Bank B (USA), it would call it a Loro account — their account with you.

Practical Application in International Banking

These accounts are critical in correspondent banking, a system that enables international trade and global payment networks.

Key uses include:

- Settlement of foreign currency transactions

- Cross-border remittances and wire transfers

- Liquidity management in multiple currencies

- FX dealing and hedging operations

- International trade finance and letters of credit

Example Workflow:

- An Azerbaijani importer pays a US exporter.

- The Azerbaijani bank uses its Nostro account in the USA to transfer USD.

- The American bank credits the exporter’s local account via its Vostro account system.

This seamless coordination between Nostro and Vostro accounts ensures speed, accuracy, and transparency in global financial settlements.

Conclusion

In international banking, Nostro, Vostro, and Loro accounts represent the three perspectives of the same relationship between banks across borders. Understanding these concepts enables financial professionals and treasurers to navigate cross-border payments, liquidity management, and correspondent relationships with greater clarity and precision.

In essence:

- Nostro = Our account with you

- Vostro = Your account with us

- Loro = Their account with you

These three pillars are the linguistic and operational foundation of global banking communication.